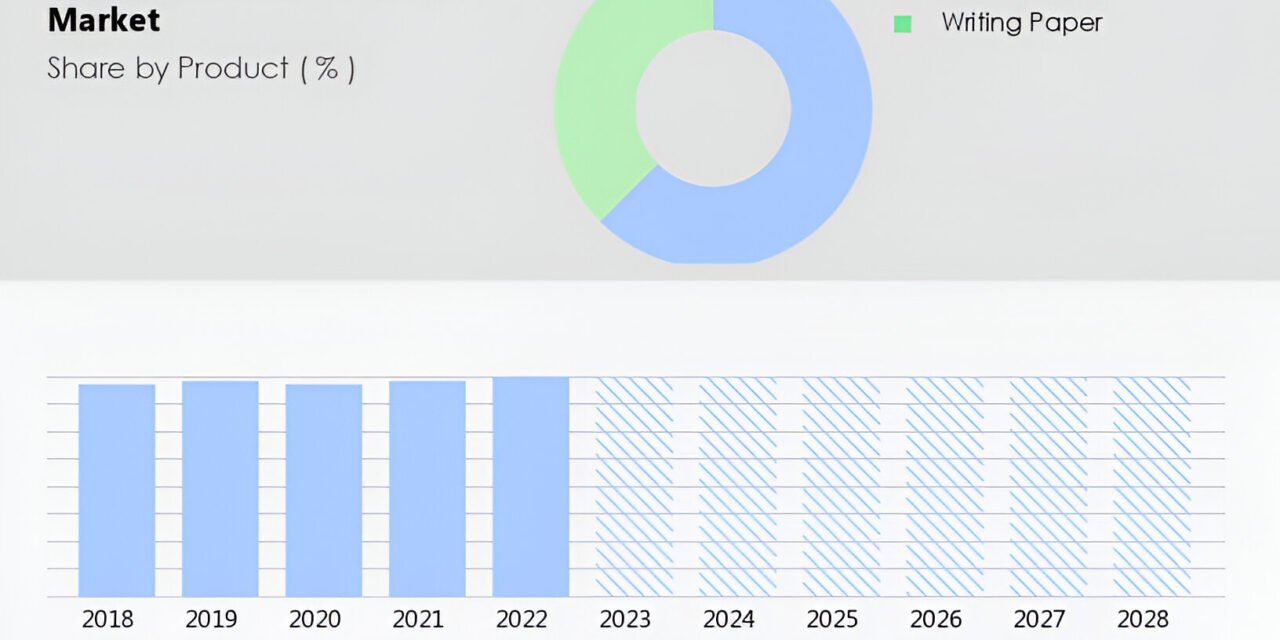

The Indian writing and printing (W&P) paper market is navigating significant challenges amidst rising raw material costs and fluctuating demand. Hardwood and softwood, critical raw materials for pulp production, have seen a sharp price increase due to heightened demand from wood-based industries and reduced output from plantations impacted during the pandemic. These cost pressures, coupled with the impact of global supply chain disruptions, have resulted in an 18-20% hike in imported wood prices, affecting the profitability of manufacturers. The industry’s dependency on wood has intensified the urgency for sustainable and cost-effective alternatives to mitigate long-term risks.

Operating margins for W&P paper manufacturers are expected to shrink by 400-500 basis points to 15-16% in the current fiscal year. This decline follows a similar contraction in the previous year, marking a sustained period of financial stress for the industry. The pressure is exacerbated by competitive pricing from imports, particularly from China and East Asia, which fulfill a substantial portion of India’s demand for uncoated and coated paper. Domestic players are struggling to maintain pricing power, further squeezing margins.

Despite these challenges, the sector remains resilient, with manufacturers focusing on efficiency improvements and leveraging deleveraged balance sheets to weather the downturn. Capital expenditures are being kept modest to maintain financial stability. Additionally, plantation initiatives over the past two years are expected to bear fruit, potentially stabilizing domestic wood prices and improving raw material availability in the coming fiscal years. This strategic focus on resource sustainability is likely to enhance the industry’s resilience in the face of future cost pressures.

Looking ahead, the W&P paper market’s revenue is projected to decline marginally by 2-3% this fiscal year, following a 6-7% drop in the previous year. However, there are signs of a gradual recovery, with operating margins expected to rebound by 300-400 basis points to 18-19% in the next fiscal year. This recovery will be underpinned by improved raw material availability, stable demand from educational and office sectors, and the industry’s adaptation to global sustainability trends. As the market stabilizes, manufacturers are also exploring innovative, eco-friendly product offerings to align with evolving consumer preferences and regulatory requirements.

{kind=link}